Smart Strategies for Saving a Down Payment to purchase a House.

Are you trying to save money for a down payment on a home you’ve always wanted to own? It can be difficult to save for a down payment, but with some clever tactics and a dedicated attitude, you can make your dream a reality. In this post, we’ll look at practical strategies for helping you save money for a down payment on a future home.

A major financial accomplishment, saving money for a down payment is one of the first stages in purchasing a property. The down payment is a portion of the home’s price that you pay upfront and can be anything between 3% and 20% or more. Even though it might seem impossible, you can amass the money required for that down payment with the appropriate plans and tenacity.

Choosing a Goal.

It’s critical to have a specific, attainable goal before you begin the process of saving for a down payment. Based on the price range of the residences you are interested in, calculate the amount you need to save. Having a clear goal will keep you motivated and concentrated while you save money.

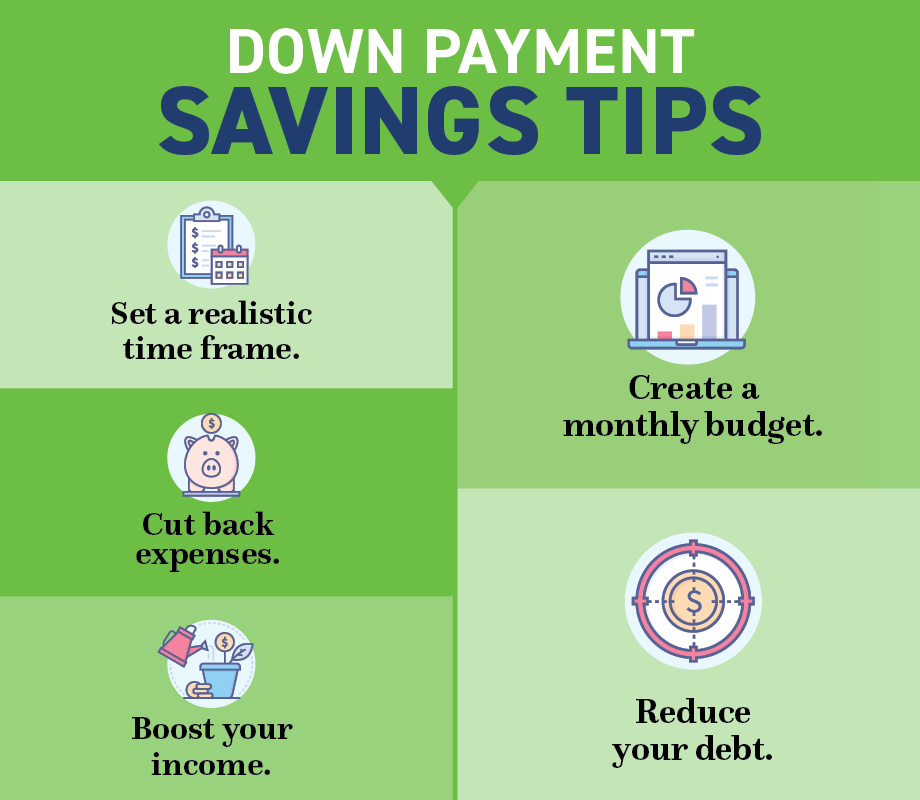

Developing a Budget.

Any successful savings plan must be built on a solid budget. To better comprehend your financial condition, examine your income and outgoing costs. Sort your expenses into necessary and unnecessary spending categories. Find areas where you may make cuts and put that money toward your down purchase savings.

Cutbacks on Costs.

A good approach to hasten the savings for your down payment is to cut back on your costs. Seek out possibilities to reduce wasteful spending. Reduce your spending on eat-out, entertainment subscriptions, and unnecessary purchases. You can get closer to your objective by saving money every day.

Increasing Revenue.

Cutting costs is important, but increasing your income can hasten the savings process. Investigate ways to increase your income, such as working a second job, freelancing, or making money from your interests. By directly allocating the additional income to your down payment savings, you can accomplish your goal sooner.

Savings Automation.

Automating your savings is one of the best strategies to accumulate a down payment. Create a scheduled automatic transfer from your checking account to a certain savings account. By doing this, a portion of your income is automatically set aside before you have the chance to spend it. It eliminates the desire to spend the money elsewhere.

Investigating Programs to Assist with Down Payments.

Look into any local programs that offer aid with down payments. These initiatives are made to assist low-income individuals and families in getting over the barrier of a down payment. Homeownership is made more accessible by them by offering grants, low-interest loans, or other forms of financial aid.

Use of Tax Benefits.

Make sure you are aware of the tax advantages of owning. You might be qualified for mortgage interest, property tax, or mortgage insurance premium deductions or credits, depending on your specific situation. To learn how these advantages can increase your savings, speak with a tax expert.

Investing for Growth You might want to put some of your savings into long-term, low-risk investments that have the potential to develop. While it’s crucial to keep the money for your down payment in reserve, making smart investments can help you amass more money over time. To determine the best investments for you given your time horizon and risk tolerance, speak with a financial counselor.

Monitoring Development.

To make sure you don’t stray from your savings objectives, keep a close eye on your progress. Track your spending, savings, and overall financial well-being using internet resources or mobile applications. Visualizing your progress can inspire you to continue saving and make improvements as needed.

Sustaining Motivation.

Persistence and self-discipline are needed to save for a down payment. Visualizing the finish line—having a spot to call your own—will help you stay focused. Celebrate progress along the road to honor your perseverance. Find supportive friends and family that appreciate the significance of your objective and surround yourself with positive influences.

In conclusion, although saving for a down payment on a future house may seem like a difficult endeavor, it is doable with the appropriate approaches. Establish clear objectives, make a budget, cut back on spending, raise your income, automate your savings, and look into aid options. Make use of tax deductions, think about making wise investments, monitor your progress, and most importantly, never lose motivation. You may take a big step toward realizing your dream of homeownership by implementing these clever tips.

FAQs

1. How much money should I put aside for a down payment?

The price range of the residences you are considering will determine how much money you should set aside for a down payment. In order to avoid paying private mortgage insurance (PMI), it is typically advised to save aside at least 20% of the home’s purchase price.

2. How much time does it take to save savings for a down payment?

Depending on your income, spending, and savings rate, it may take you longer to save for a down payment. Within a few years, a down payment can be saved with the appropriate planning and disciplined saving.

3. Is it possible to use gift money as a down payment?

You can utilize gift money for your down payment, yes. To guarantee the legitimacy of the source of the cash, however, there can be certain criteria and paperwork requirements.

4. Is there a drawback to a lower down payment?

Private mortgage insurance (PMI), which raises your monthly mortgage expenses, may be necessary if you have a low-down payment. Additionally, it indicates that you have a larger loan-to-value ratio, which may affect the approval of your loan or lead to higher interest rates.

5. Can the seller and I agree on a down payment amount?

You can bargain over other components of the home-buying process, such as closing costs or repairs, even if it is uncommon to directly negotiate the down payment amount with the seller. It’s preferable to seek advice from your real estate agent or lawyer.